Rapid food inflation is often concerning for various stakeholders in the food system. Therefore, stable food prices directly speak to food access; and it has been shown that rapid food inflation has often lead to social unrests around the globe. From a production perspective, this could signal good news due to price growth often being a symptom of economic prosperity and an increased appetite of consumers to spend. This ultimately provides price support that is also transmitted to the producer level.

Over the past 18 months, South Africa has experienced significant food inflation – mostly related to production and economic factors, but not as a result of demand growth. This article explores the causes of increases in retail prices over the corresponding period to highlight the dynamics at play for all stakeholders involved in food production (and consumption).

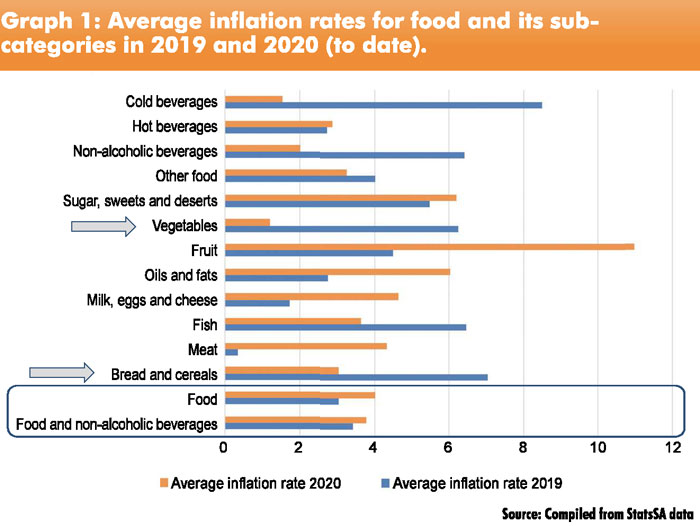

In 2019, food inflation dynamics already painted a picture of the South African consumer’s income being under severe pressure. A key feature of food inflation during 2019 was that it was driven by price increases in non-premium products such as staples and vegetables (see arrows in Graph 1). This, in turn, provided price support in these categories on the back of a strong demand, with consumers seeking value for money.

Since then, economic conditions and the disposable income have deteriorated even further due to the COVID-19 pandemic and its associated restrictions with the lockdown. To add insult to injury, the outbreak of the pandemic and its associated lockdown resulted in disruptions in supply chains and changes in consumer expenditure patterns, which sustained relatively high inflation levels despite the strain that consumers were under. Within this context, this article explores what happened to food prices during 2020 and what we could expect for the next six months.

Since then, economic conditions and the disposable income have deteriorated even further due to the COVID-19 pandemic and its associated restrictions with the lockdown. To add insult to injury, the outbreak of the pandemic and its associated lockdown resulted in disruptions in supply chains and changes in consumer expenditure patterns, which sustained relatively high inflation levels despite the strain that consumers were under. Within this context, this article explores what happened to food prices during 2020 and what we could expect for the next six months.

Price trends during 2020

From Graph 1 (on page 38) it should be apparent that the main contributors to food inflation in 2020 were fruit (11%), sugar and confectionery (6,2%), oils and fats (6%), milk, eggs and cheese (4,6%), and meat (4,3%).

- In the case of fruit, prices recorded double-digit year-on-year (YoY) increases due to low volumes. Fruits such as bananas had a significantly lower yield than normal, due to the cold winter. Local citrus volumes, in turn, were lower on the back of substantial export volumes early in the season, driven by the depreciation of the rand.

- The prices of sugar and confectionery products increased due to increases in the underlying producer price of sugar, combined with strong demand growth during the months of lockdown. This can be explained by an increased household consumption of sugar for baking and cooking purposes. During the lockdown, the demand for carbonated drinks also increased significantly due to the unavailability of alcoholic beverages, thereby increasing the demand for sugar.

- Oils and fats’ prices have increased considerably on the back of increased parity prices of soybeans and sunflowers since March 2020. This increase was, in turn, driven by a weak(er) rand.

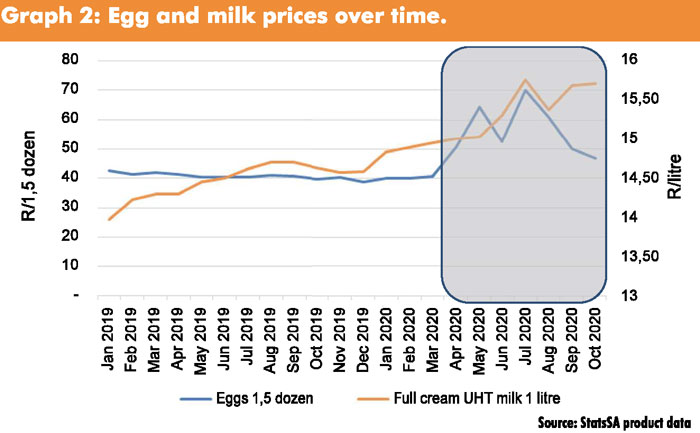

- The prices of milk, eggs and cheese are considered in one category in food inflation monitoring. In this category egg prices rallied during April and May due to consumer stockpiling (see Graph 1). This disruption in demand allowed for a correction in prices to ease some of the pressure that producers were facing due to increasing production costs, combined with limited increases in output prices. Although egg prices did come down from the highs experienced between May and July 2020, prices were still almost 18% higher in September 2020 compared to that of September 2019. Retail milk prices have also increased significantly since the beginning of the lockdown (see the grey area in Graph 2). The producer price index (PPI) on unprocessed milk has been increasing rapidly since the beginning of 2020, suggesting that the underlying cost of unprocessed milk is driving the higher retail price.

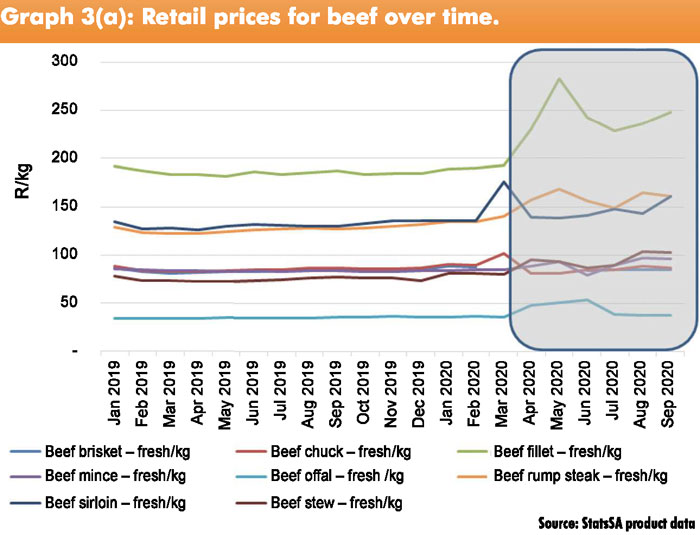

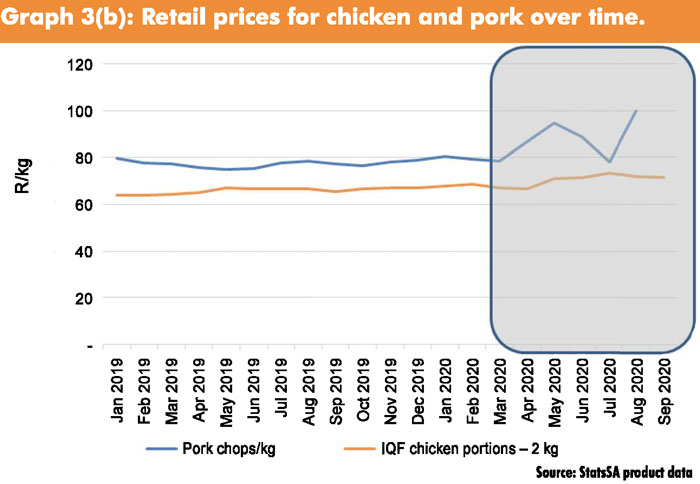

- In the case of meat, prices in 2020 are measured against a relatively low base because of the effect of foot-and-mouth disease on red meat prices during 2019. The 6,2% increase should therefore be seen in this context. Graph 3(a) and Graph 3(b) show retail price trends for selected meat products since January 2019.

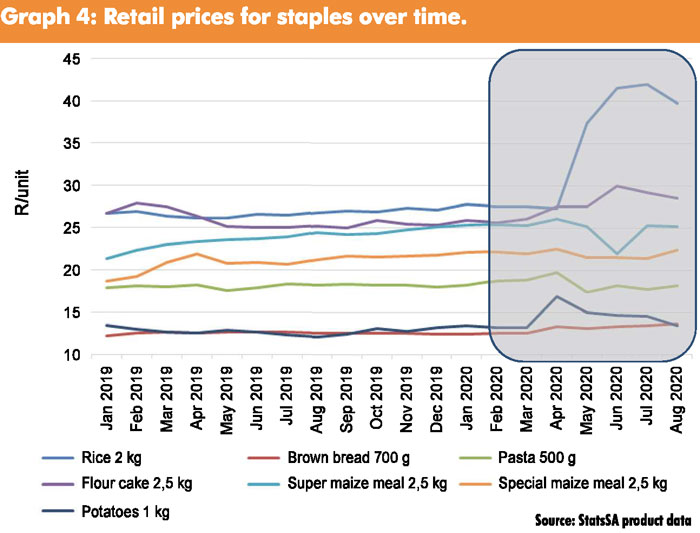

South Africa’s national lockdown Level 5 has shown that consumers tend to lean towards products (such as pasta, cake flour and rice) with extended shelf lives in times of crises. This, together with the severe financial pressure COVID-19 has inflicted on households, caused consumers to switch to cheaper staple food options.

South Africa’s national lockdown Level 5 has shown that consumers tend to lean towards products (such as pasta, cake flour and rice) with extended shelf lives in times of crises. This, together with the severe financial pressure COVID-19 has inflicted on households, caused consumers to switch to cheaper staple food options.

Panic buying led to an almost immediate increase in the prices of staple foods. April/May showed the price of rice significantly increasing (36,7%), with a further increase during May/June (11%). This can be ascribed to trade restrictions, as South Africa is dependent on rice imports. Although the price of rice has since started to decrease, it is still 48,7% higher year on year.

Graph 4 shows retail prices for various staples. The price of a 700 g brown bread increased with 6%

between March and April. The price of brown bread has increased with 8,9%, and is still increasing. This could again be ascribed to exchange rate movements, as South Africa is a net importer of wheat.

The price of pasta has been highly volatile since 2019. March/April saw the price of pasta increase with 4,7%, decreasing with 11,6% during April/May and increasing again with 4,1% during May/June. The year-on-year price of pasta has, however, remained constant (decreasing by 0,1%).

The price of pasta has been highly volatile since 2019. March/April saw the price of pasta increase with 4,7%, decreasing with 11,6% during April/May and increasing again with 4,1% during May/June. The year-on-year price of pasta has, however, remained constant (decreasing by 0,1%).

The price of cake flour increased by 5,8% in March/April, with a further increase of 9% in May/June. The year-on-year price of cake flour has increased by 13,2%. The price of super maize meal has been steadily increasing since 2019 (2,9%). This is, however, in line with the current inflation rate for breads and cereals, driven by increases in underlying parity prices.

Another supply shock includes the unusually cold winter in Limpopo during the early part of the potato harvest, which resulted in South Africa’s potato prices skyrocketing (27,8% during March/April).

2020 and beyond

At the hand of the above, it is evident that food prices can change rapidly as a result of exogenous shocks. It is clear from the graphs that the COVID-19 pandemic and its associated lockdowns resulted in disruptions which ultimately manifested in retail prices. These disruptions ranged from supply chain disruptions to severe changes in consumption patterns.

In some cases, as with oilseeds, the changes in prices are largely as a result of exchange rate dynamics, where the rand depreciated as a result of our sovereign credit rating downgrade and general risk averseness towards developing economies in times of crises.

As we move into levels with less restrictions, it seems that prices are correcting from the high levels apparent during the hard lockdown. Informal discussions with retailers and producer organisations relay that food consumption patterns seem to have normalised.

The big uncertainty that affects food prices going forward is the exchange rate. Second national lockdowns and elections in the Northern Hemisphere could affect the global economic recovery. This could ultimately cause the rand to depreciate further and rapidly, which would push food inflation to higher levels.

References

- Kelly P, 2016. Analysis: South Africa’s CPI reveals how volatile inflation hurts the poorest. Available at: https://www.dailymaverick.co.za/article/2016-04-28-analysis-south-africas-cpi-reveals-how-volatile-inflation-hurts-the-poorest/#.VzGS-uJ95hF [24 September 2020]

- Rangasamy L, 2010. Food inflation in South Africa: Some implications for economic policy. South African Journal of Economics, 79(2), pp. 184 – 201

- SAGIS, 2020. Food prices – Statistics SA. Available at: https://www.sagis.org.za/food_stats%20sa.html [30 June 2020]

- StatsSA, 2020. Consumer Price Index, September 2020. Available at: http://www.statssa.gov.za/publications/P0141/P0141June2020.pdf [23 September 2020]

{kind=link}