The NWK Limited external factors report provides an overview of the main external factors that NWK and its clients are exposed to at a specific point in time. This report opts to aid in a timely basis to foresee external market and other factors that may have an impact on any business and clients. The main focus of this document is to have a closer look at external factors that can affect any business and our customers.

Executive summary

Fortunately, the inflation rate cooled down to 5,3% in February 2024. Retail trade decreased with 0,8% in February compared to a year-to-year basis. The unemployment rate increased slightly to 32,1% in the fourth quarter of 2023. The GDP growth for the fourth quarter was 0,1%, up from a 0,2% decline in the previous quarter. The Policy Uncertainty Index moved further into negative territory from 65,5 to 65,8 points in Q1.

The National Agricultural Marketing Council (NAMC) projected the ending stock for 30 April 2024 of white and yellow maize to be less than the 2022/2023 season. According to the Crop Estimation Committee’s second forecast the three main maize producing areas, namely the Free State, Mpumalanga and North West are expected to produce 79% of the 2024 crop.

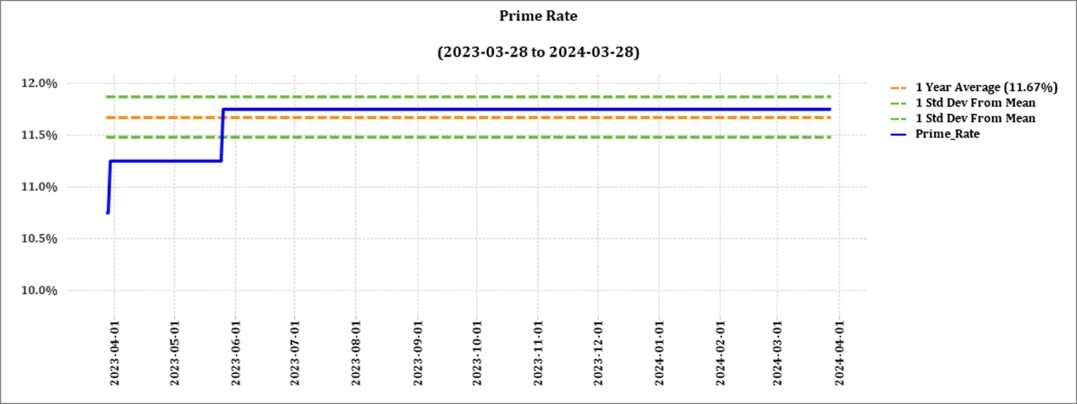

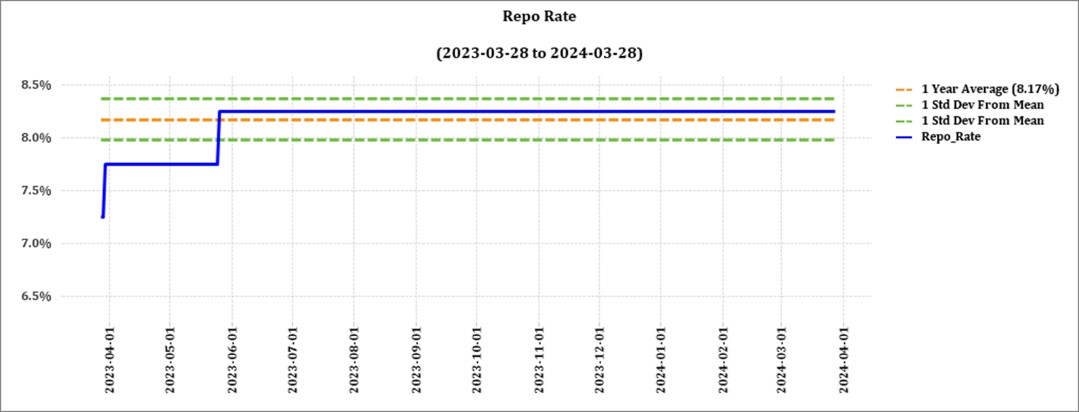

During the previous Monetary Policy Committee (MPC) meeting held on 27 March the committee once again decided that interest rates will remain unchanged. The repo rate is currently 8,25% and the prime rate 11,75%.

Load shedding poses long term risks for the agricultural sector on a supply and input cost level. Cost-effective and sustainable alternative solutions must be considered in order to reduce the dependency on Eskom for electricity. With fuel prices sky rocketing and producers being more and more reliant on generators for electricity this is a disaster.

Business climate: Key risk drivers

A few highlights regarding certain risk drivers are mentioned below.

According to Trading Economics South Africa’s annual inflation rate cooled down to 5,3% in March from 5,6% in the prior month, verging on the upper limit of the South African Reserve Bank’s inflation target range of 3% to 6%.

Brent crude oil monthly average prices decreased by $3,35 per barrel from January to February. South Africa’s retail trade decreased with 0,8% in February compared to the same month a year earlier. According to Statistics SA, South Africa’s unemployment rate rose slightly to 32,1%.

The GDP growth rate rose to 0,1% on quarter for the fourth quarter in 2023. Six of the ten activities picked up in the first quarter. The transport industry contributed the most with a growth of 2,9%. The transport industry contributed the most with a growth of 2,9%.

The local Safex price was considered to be at break-even point according to February 2024 white maize spot prices. According to the World Bank’s grain price index maize prices declined 18% in the third quarter. Ukraine had a bumper harvest in 2023, with maize production increasing by 4% compared to 2022.

Despite repeated attacks on its ports, grain shipments continued to flow out of Ukraine, primarily through the Danube River. Global supply of maize and soybeans for the 2023/2024 season is forecast to be much higher than the 2022/2023 season.

Adverse weather patterns can reduce yields and also affect the Safex price; to many producers’ relief the El Niño is nearing its end and ENSO-neutral conditions are predicted for late autumn 2024 with some climate models even predicting a La Niña by late winter. The impact of El Niño on yields and prices varies across geographies, crops, and seasons. Historically, El Niño is associated with rising prices of agricultural commodities. For example, El Niño reduces the global average yield for maize by 2,3% while it increases soybean yields by 3,5% (Iizumi et al. 2014). The solar cycle is approaching its turning point in May 2024, which indicates less rainfall predicted for coming years.

The iron ore price saw a decrease of $15,46 per metric ton from February to March. Prices for iron ore cargoes with a 63,5% iron ore content for delivery into Tianjin fell to $102 per tonne in April, the lowest in 10 months, setting a broad-based decline for ferrous metals as muted demand in top consumer China was magnified by ample supply.

The Policy Uncertainty Index (PUI) moved further into negative territory from 65,5 to 65,8 points in Q1. In addition to the well-known global risks and uncertainties the 2024 election outcome is also weighing on investors and the markets. The PUI is the net outcome of positive and negative factors influencing the calibration of policy uncertainty over the relevant period. It is seen to have important implications for business confidence and the investment climate in the country.

Sources

https://tradingeconomics.com/south-africa/inflation-cpi

https://tradingeconomics.com/commodity/brent-crude-oil

https://tradingeconomics.com/south-africa/unemployment-rate

https://www.agbiz.co.za/content/open/21-august-2023-agri-market-viewpoint-747

https://tradingeconomics.com/south-africa/gdp growth#:~:text=South%20Africa%20GDP%20Grows%201.2,expectations%20of%20a%200.7%25%20growth

https://www.statssa.gov.za/?page_id=737&id=1

https://tradingeconomics.com/commodity/iron-ore

https://openknowledge.worldbank.org/server/api/core/bitstreams/27189ca2-d947-4ca2-8e3f-a36b3b5bf4ba/content

PUI_2024Q1.pdf

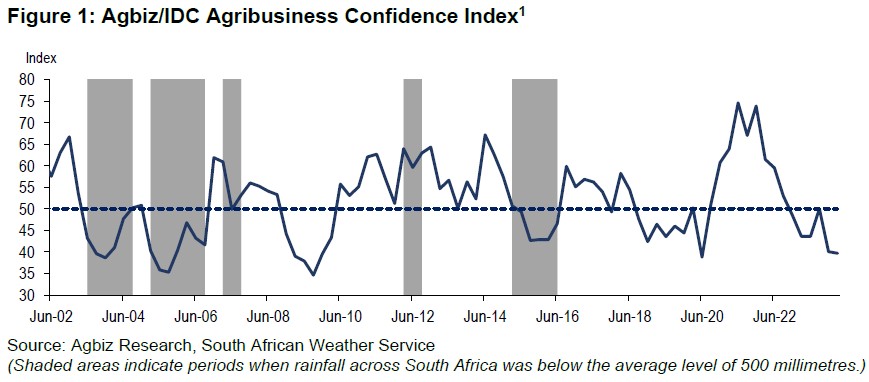

Agbiz/IDC ACI deteriorated further in Q1, 2024

The Agricultural Business Chamber (Agbiz) quarterly conducts a survey in order to create an Agribusiness Confidence Index (ACI). The Agbiz/IDC ACI, which was released on 25 March 2024, reflects the perceptions of at least 25 agribusiness decision-makers on the ten most important aspects influencing a business in the agricultural sector.

These ten aspects are:

- turnover;

- net operating income;

- market share;

- employment;

- capital investment;

- export volumes;

- economic growth;

- general agricultural conditions;

- debtor provision for bad debt; and

- financing cost.

These aspects are used by agribusiness executives, policymakers and economists to understand the perceptions of the agribusiness sector. It also serves as a leading indicator of the value of the agricultural output while providing a basis for agribusinesses to support their business decisions.

After deteriorating by 10 points to 40 in Q4 2023, its lowest level since Q2 2020 at the height of the pandemic, the Agbiz/IDC Agribusiness Confidence Index (ACI) was unchanged in Q1 2024. The Q1 2024 reading is below the neutral 50-point mark, implying that South African agribusinesses remain downbeat about business conditions. This pessimism emanates from mostly the same factors as in recent surveys, which are yet to be addressed, and new challenges on the weather front.

These include the ongoing El Niño induced drought that is devastating the summer grains and oilseed regions, persistent inefficiencies at the ports, poor rail and road infrastructure, and the worsening municipal service delivery. The rising crime, lingering animal disease challenges, uncertain policy environment ahead of the elections, persistent episodes of load-shedding and increased geopolitical uncertainty also remain top-of-mind challenges for agribusinesses. This survey was conducted in the first three weeks of March, covering businesses operating in all agricultural subsectors across South Africa.

The graph below shows the Agribusiness Index from 2002 up to January 2024.

The ACI is comprised of ten subindices, of which three declined in the first quarter of 2024, while the rest showed mild improvement. Here is the detailed view of the subindices.

The turnover subindex was down by 14 points from Q4 2024 to 52. This deterioration in sentiment reflects the expectations of the poor summer grains and oilseed harvest in an environment where the input costs remain relatively elevated. This illustrates not only the pressures in the summer crop regions but also the respondents in the livestock industry, who are also challenged by the relatively higher input costs.

- The sub-index measuring the volume of export sentiment fell further by 7 points to 35 in Q1 2024. This deterioration in sentiment signals the potential decline in export volumes this year from a record export of US$13,2 billion in 2023. The major challenge is a potentially poor summer grains and oilseed harvest, while the fruit, wines and meat volumes may remain decent. Moreover, the ongoing worries about underperforming ports and railways also added to the pessimism.

- The general agricultural conditions subindex fell by 22 points to 18 in Q1 2024, the lowest level since the first quarter of 2016, the time of the last intense El Niño cycle that caused widespread devastation in South Africa. These results are not surprising and mirror the damage the heatwave and the dryness since the start of February has caused in the summer grains and oilseed-producing regions of South Africa, with crop harvest forecasts, also set to be lowered notably in the coming months.

Mild improvements

- The net operating income subindex, typically aligned with the turnover, improved slightly by one point from the previous quarter to 48 in Q1 2024. The agribusinesses that primarily operate in financial services were behind this slight improvement.

- The market share of the agribusiness subindex is up 6 points from Q4 2023 to 59 in Q1 2024. Except for the respondents in the inputs business, which showed an improvement, most held a generally unchanged view from the previous quarter.

- The employment subindex was up by 3 points from Q4 2023 to 50. This was a surprise given the current challenging agricultural production level. It is possible that the employers’ views were influenced by the robust results of Q4 2023, where 920 000 people were employed in primary agriculture, which is 7% up year-on-year and well above the long-term agricultural employment of 793 000.

- The capital investments subindex improved by 7 points from Q4 2023 to 50. This likely reflects the investments in alternative energy sources as the sector continues to invest in mitigating against the effects of load-shedding.

- The general economic conditions subindex recovered by 20 points to 30 in Q1 2024, still far from the neutral point mark of 50. This slight recovery in the mood about the economic conditions could be linked with expectations of a reduction in load-shedding this year, and it is broadly consistent with improvements in various market analysts’ GDP forecasts for 2024.

- The subindices of the debtor provision for bad debt and financing costs are interpreted differently from the abovementioned indices. A decline is viewed as a favourable development, while an increase signals growing financial strain. In Q1 2024, the debtor provision for bad debt was down by 9 points to 27, which is a favourable development. Meanwhile, the financing costs indices increased by 14 points to 27, signalling that agricultural firms are still worried by the elevated interest rate in an industry where farm debt is just over R200 billion.

Concluding remarks

After a few years of solid activity, South Africa’s agricultural sector faces a daunting year ahead, and the Agbiz/IDC ACI’s Q1 results reflect this challenging outlook.

‘Although weather-related risks are a major concern for this year, there remain aspects that policymakers, collaboratively with the private sector, could tackle to unlock the long-term growth potential of South Africa’s agriculture.

These include addressing the weakening municipalities, deteriorating roads, animal diseases, efficiency in the registration of new agrochemicals and seeds, rising crime, inefficient logistics, and persistent load-shedding,’ says Wandile Sihlobo, chief economist of the Agricultural Business Chamber of SA (Agbiz).

‘Still, with the elections ahead of us, it is unclear if there will be a serious focus on policy matters in the months ahead,’ added Sihlobo.

Source: www.agbiz.co.za, Issued by: Wandile Sihlobo, Chief Economist (Agbiz) March 2024.

Weather and climate

NATIONAL ASSESSMENT

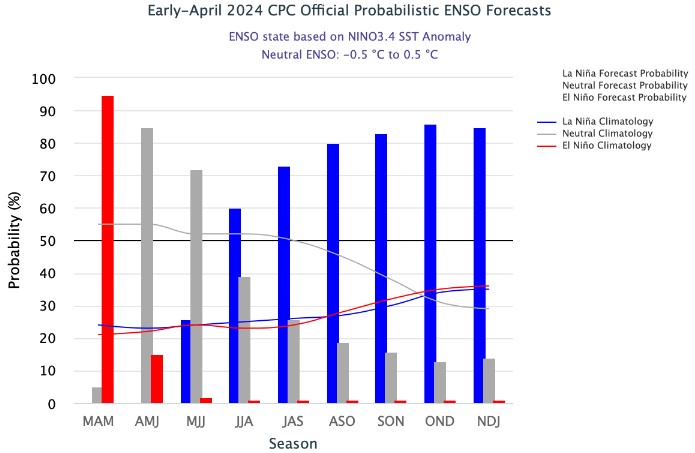

The El Niño-Southern Oscillation (ENSO) is now (early April) in an El Niño phase at 95%. The chance of an El Niño still being present from April to June 2024 declines dramatically to 15%.

The latest Climate Watch issued by the SA Weather Service predicts below-normal rainfall over most areas of the western part of the country, while the outlook for rainfall over the eastern parts has lower probabilities assigned to the relevant rainfall category (below-normal or above-normal) with some areas characterised by no clear signal.

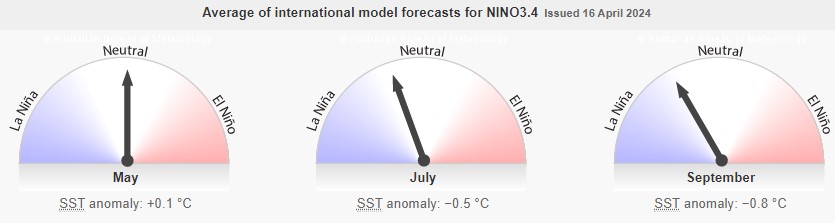

The Burea’s ENSO Outlook is at El Niño. Climate model outlooks suggest El Niño has peaked and is declining, indicating a return to neutral in the southern hemisphere autumn 2024.

The ENSO Outlook will remain at El Niño status until this event decays, or signs of a possible La Niña appear. The current SSTs for May to September range from +0,1°C to -0,8°C. Persistent values warmer than +0,8°C are typical of an El Niño.

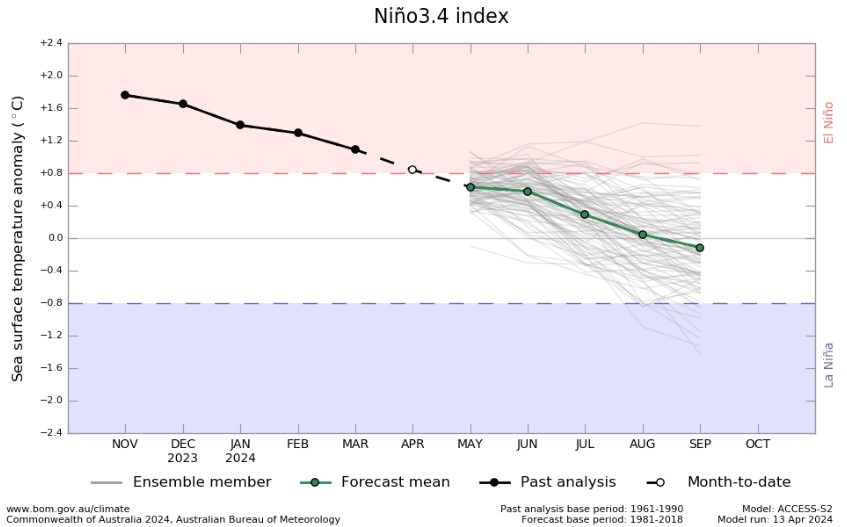

According to the graph below, ENSO is in an El Niño phase, and ocean temperatures near the equator are slowly starting to get cooler. The downward trajectory of the graph shows that the El Niño has reached its peak and more rain can possibly be expected later during the year as temperatures start to subside.

Source: Australian Government – Bureau of Meteorology

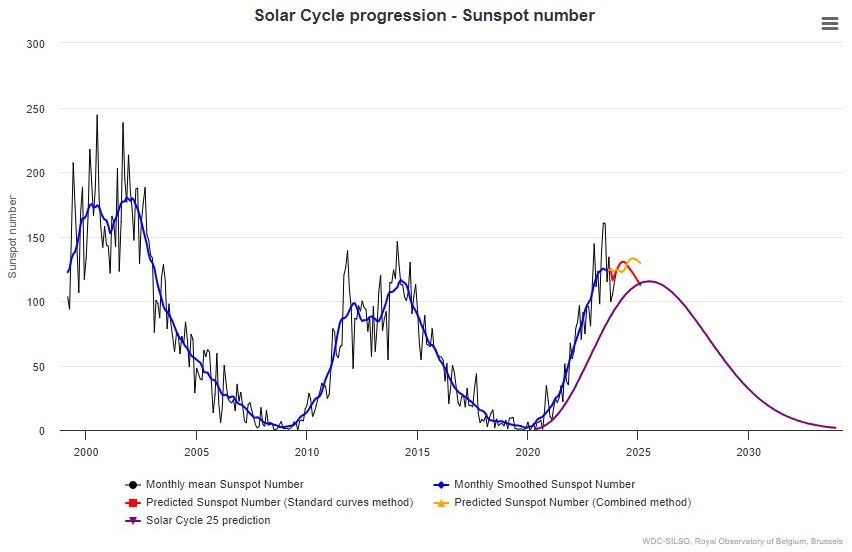

SUNSPOTS

Sunspots are darker, cooler areas on the surface of the sun that arise due to disturbances in the sun’s magnetic field. Every 11 years, the number of spots dotting the surface of the sun increases and decreases and forms the solar cycle.

Sources

https://www.sciencedirect.com/science/article/abs/pii/S136468262200116X#:~:text=It%20was%20observed%20that%20rainfall,an%20increasing%20effect%20on%20rainfall

https://www.space.com/solar-cycle-frequency-prediction-facts May 27,2022

https://eos.org/articles/why-did-sunspots-disappear-for-70-years-nearby-star-holds-clues 10 June, 2022

According to science direct the rainfall rate is directly related to the sunspot number but shows different characteristics during solar maximum years. Though a lag correlation exists between sunspot number and rainfall, sunspots have an increasing effect on rainfall. Studies show that the more sunspots are present the higher the rainfall and the less sunspots the lower the rainfall.

ENSO occurs at irregular interval between three and seven years causing global climate system variation. Considering this event occurs periodically, it might be triggered by the eleven years of solar cycle as an energy source.

The graph below shows the eleven year solar cycles since before the 2000s. As the graph is in an upward trajectile higher rainfall can be expected – La Niña. As the graph reaches its turning point and moves in a downward trajectile less rainfall is expected characteristic of an El Niño.

The last three years were La Niña years and as the graph is approaching its forecasted turning point in May 2024 an El Niño can be expected for the coming years. ENSO indicators are currently at at El Niño and it is expected to continue through to autumn. In December 2023 the actual sunspot numbers were higher than the predicted values and in the predicted range, for January to March 2024 the actual was higher than the predicted values as well as the predicted range indicating that the current phase of increasing sunspots is associated with the possibility of more rainfall, while a decreasing phase typically corresponds to less rainfall.

One could assume that ENSO-neutral conditions start to develop as the number of sunspots is close to reaching their maximum, the turning point on the graph, and then turn towards El Niño as the sunspots get less and the graph move downwards.

Market risk

GRAIN MARKET ANALYSIS

• Ending stock – national

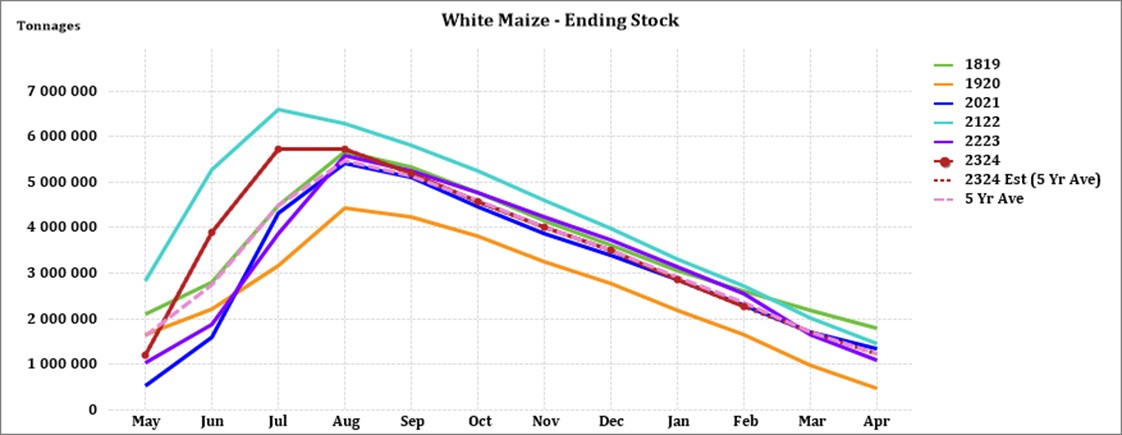

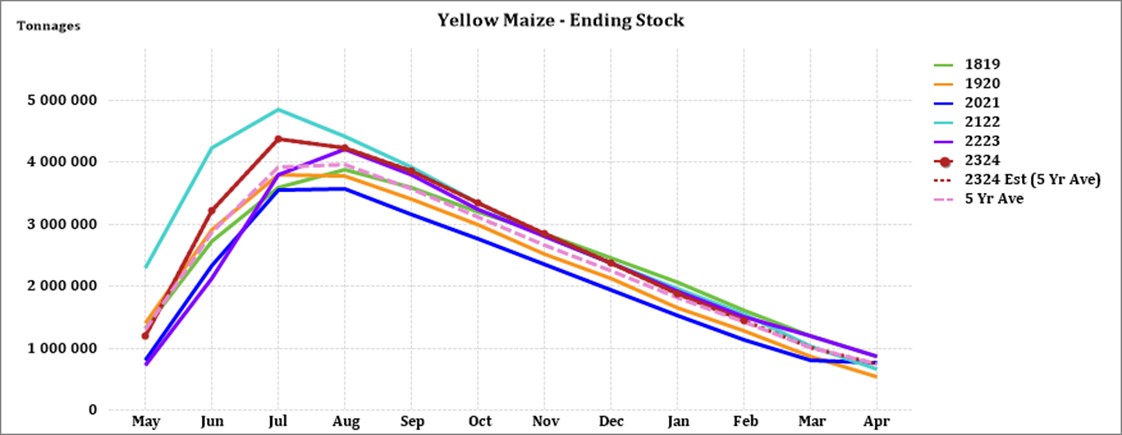

Ending stock data is gathered from the NAMC. The estimates are reassessed and reported by the Grain and Oilseeds Supply and Demand Estimates Committee. The following is the projected ending stock for April 2024 in tonnages for the 2023/2024 season:

- White maize => 1 546 400 t

- Yellow maize => 1 131 757 t

The following is a summary of September 2024 ending stock estimates for the 2023/2024 season:

- Wheat => 437 784 t

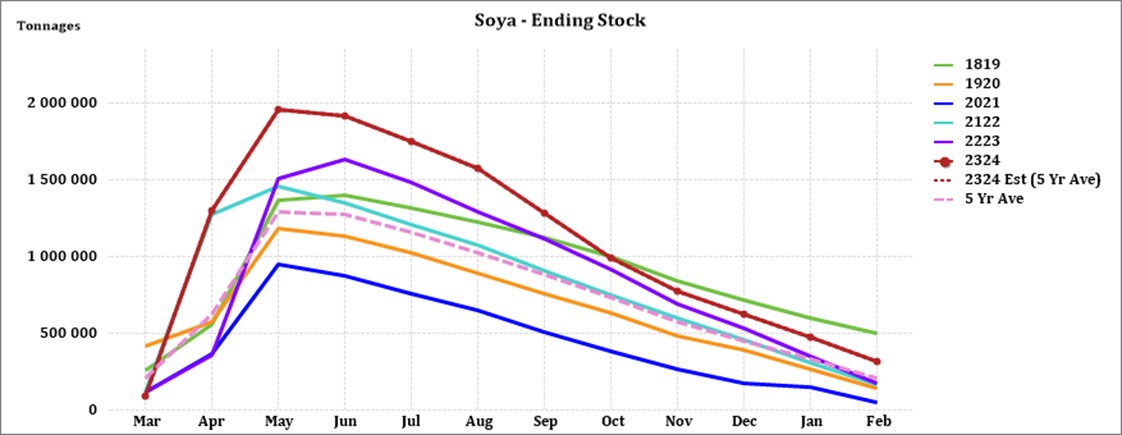

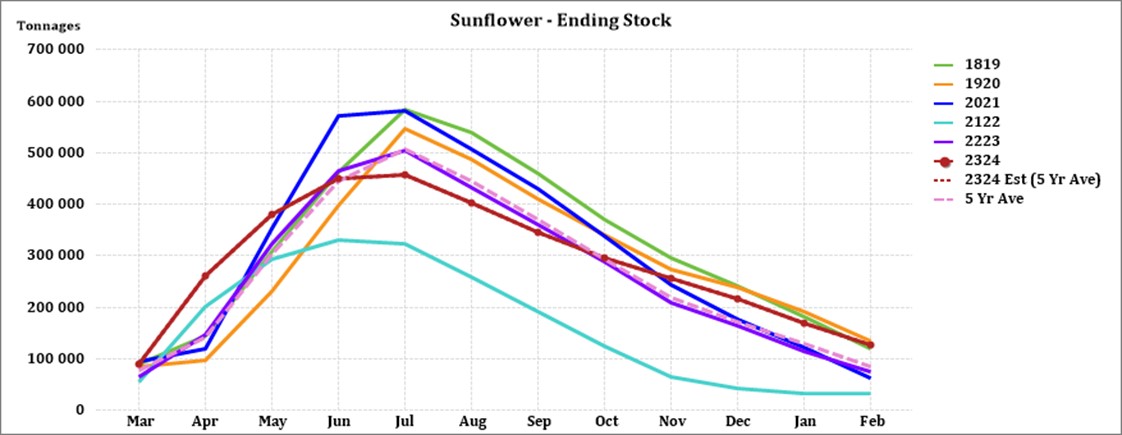

The following is a summary of the February 2024 projected final ending stock for the 2023/2024 season:

- Sunflower => 126 577 t

- Soybeans => 294 147 t

- Sorghum => 70 046 t

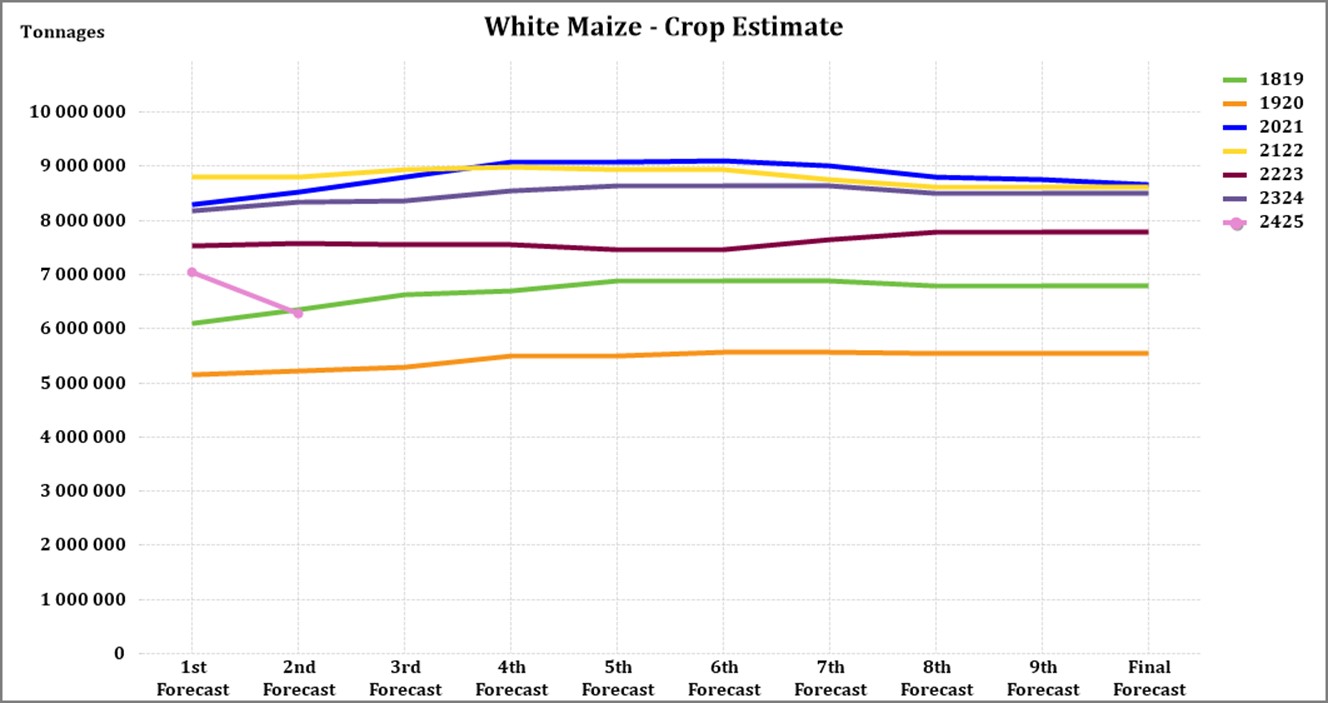

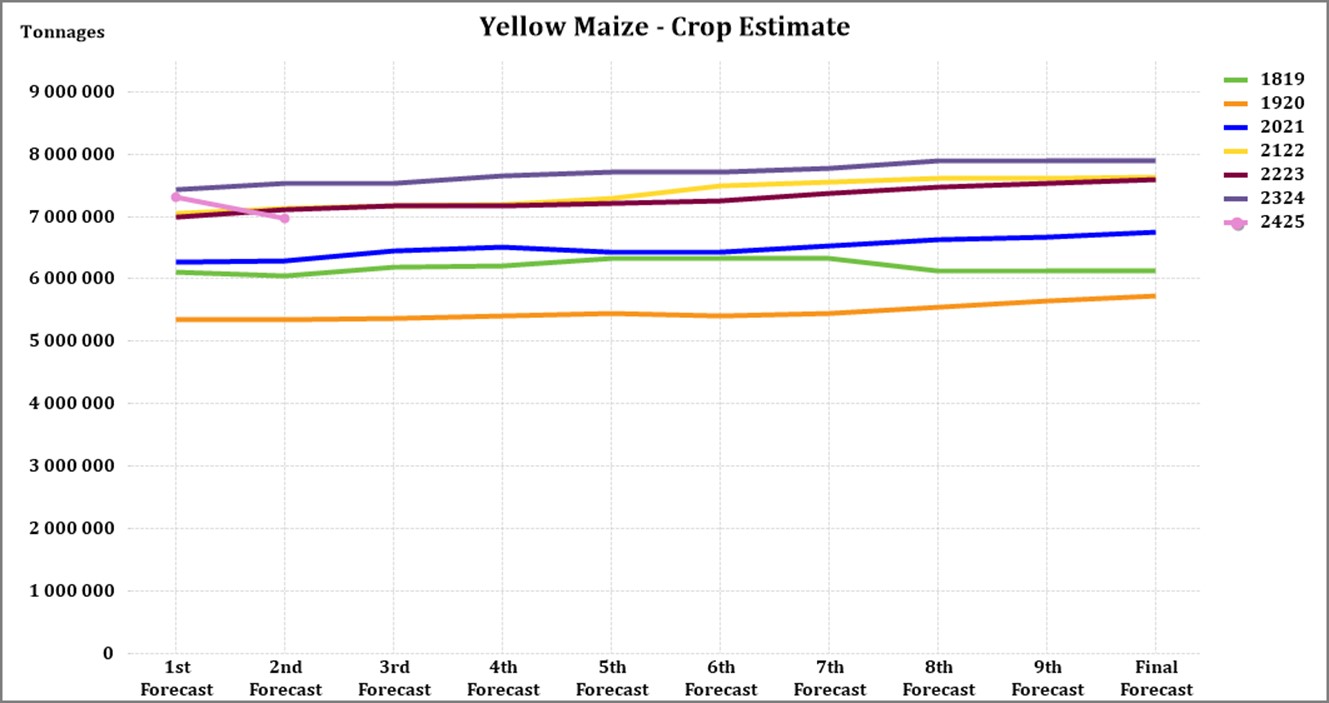

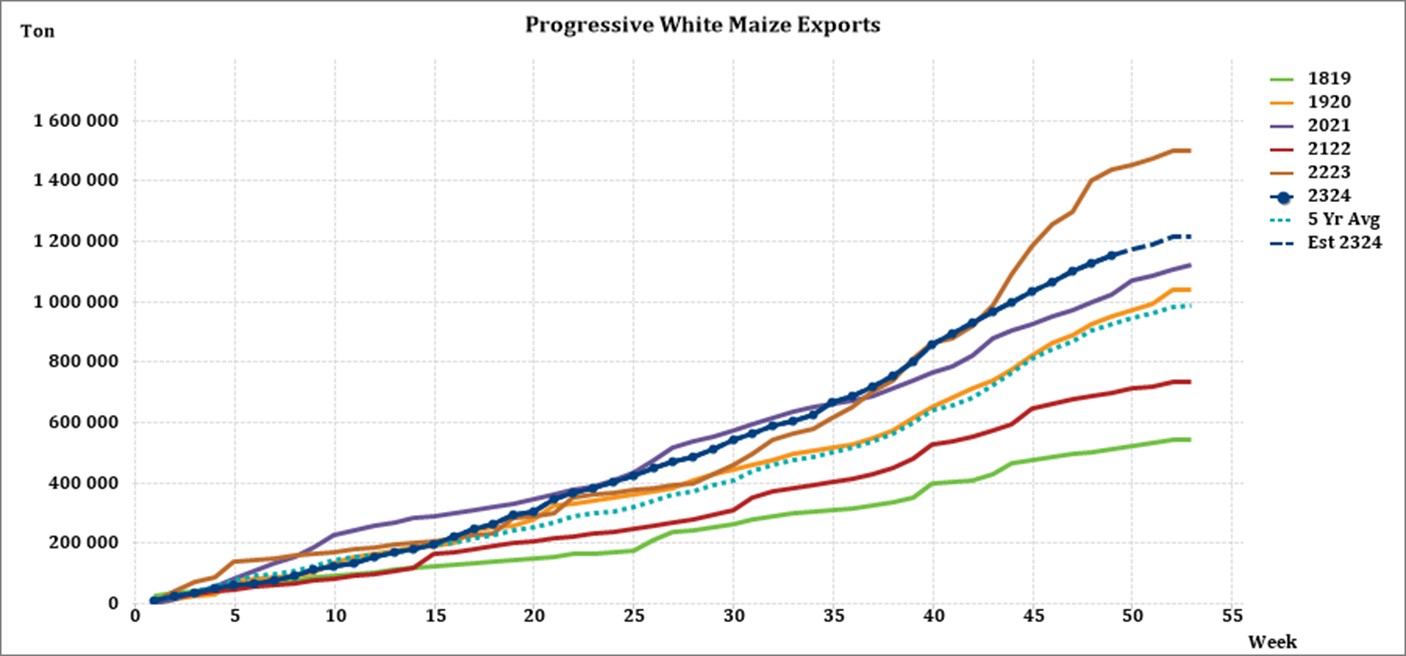

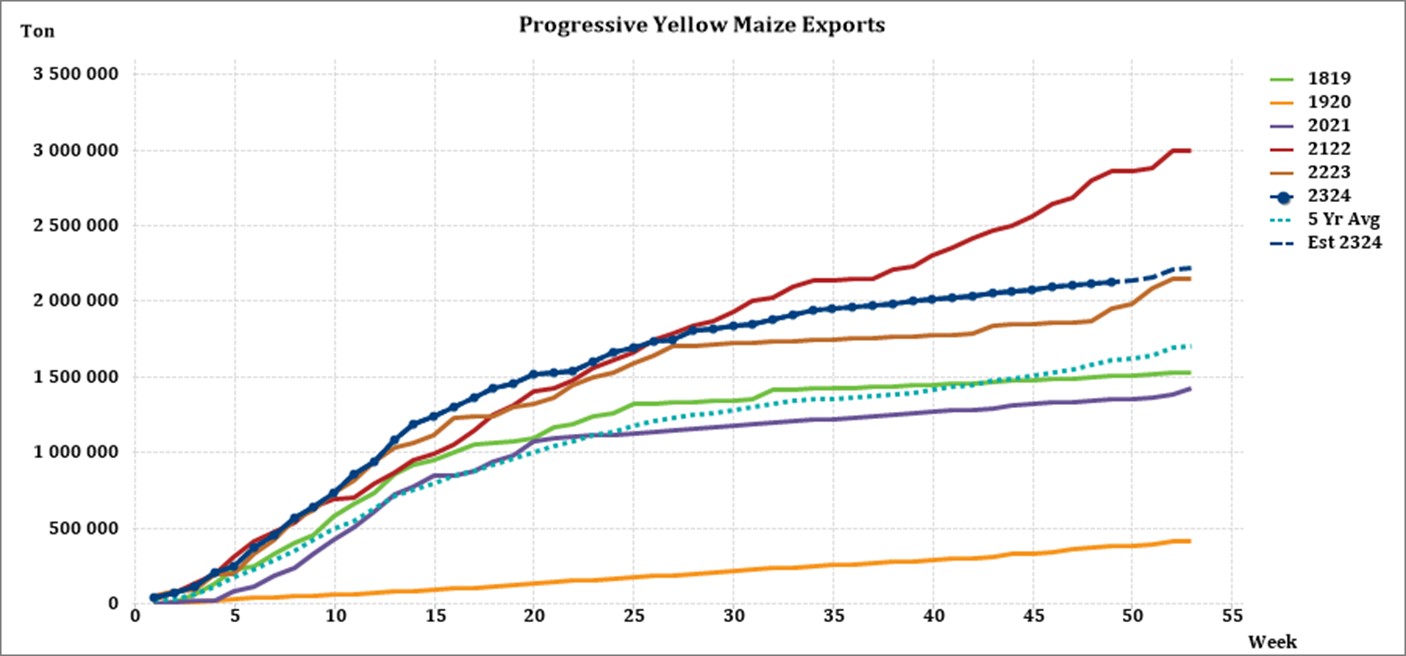

The graphs below show the predicted ending stock for the different commodities according to SAGIS data. A five-year average has been calculated to determine the estimated ending stock for the current season. The predicted white maize in April 2024, is 152 578 t more than the final for the 2022/2023 season. Yellow maize shows a 134 761 t decrease in ending stock compared to the previous season.

Source: Sagis

Source: Sagis

Source: Sagis

The forecasted soybean ending stock for February 2024 is 147 900 t more than February 2023.

Source: Sagis

The forecasted sunflower ending stock is 53 197 t more than the previous season ending stock.

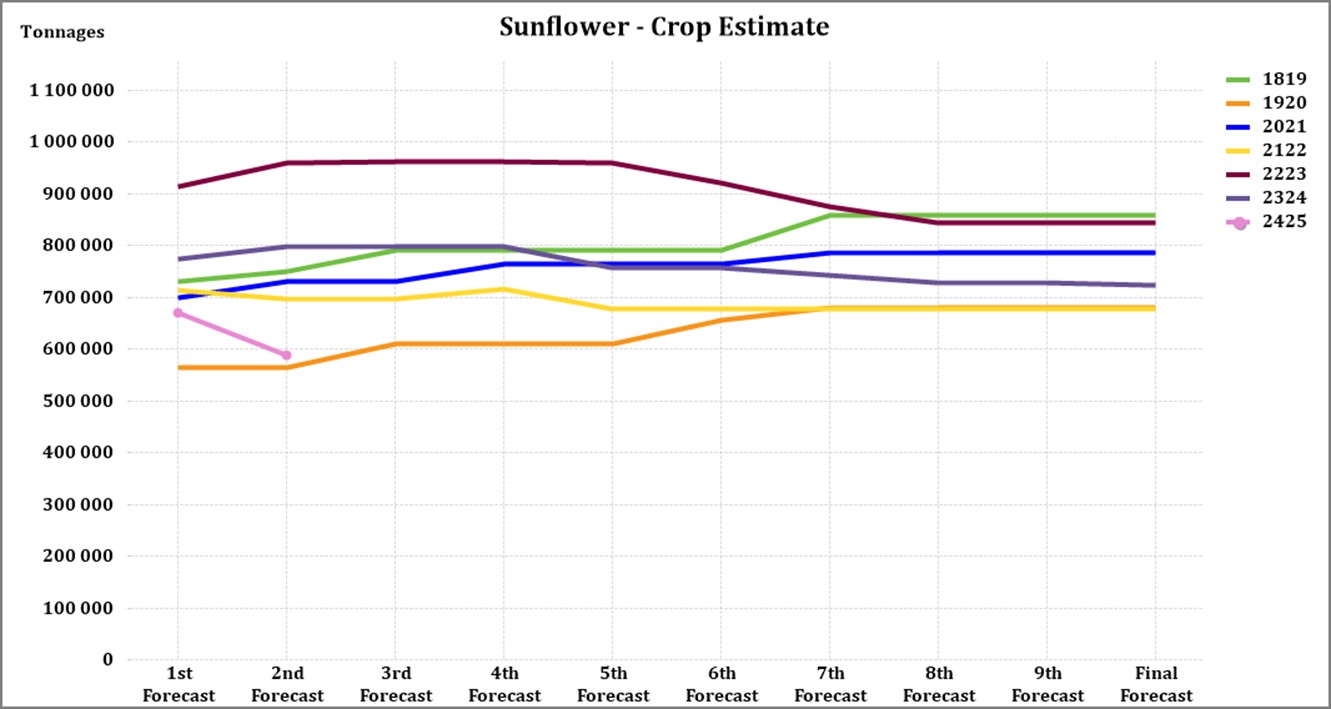

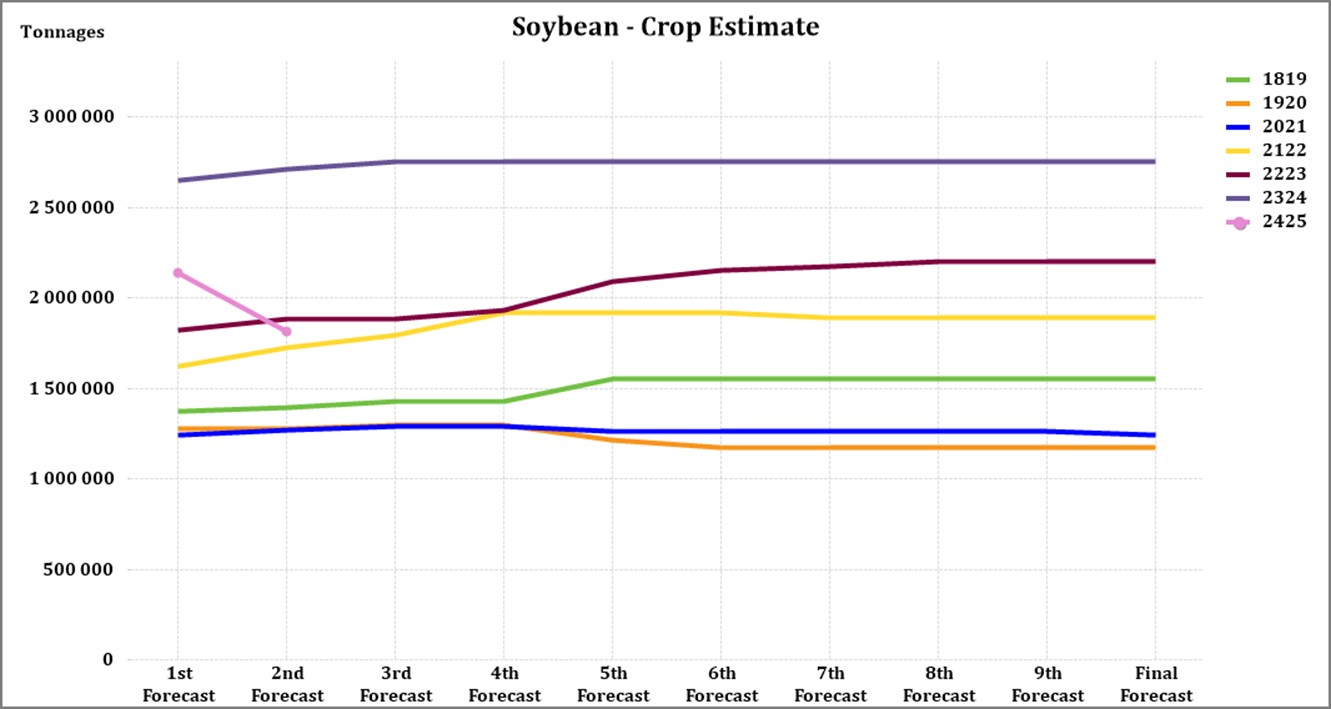

Crop estimations

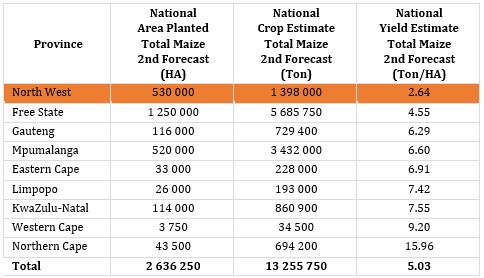

According to the Crop Estimate Committee (CEC) production forecast for 2024, the area estimate for maize is 2,636 million ha, which is 1,9% less than the actual 2,586 million ha planted for the previous season.

Source: CEC (Crop Estimates Committee)

Source: CEC (Crop Estimates Committee)

Source: CEC (Crop Estimates Committee)

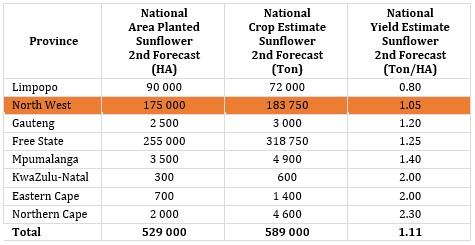

The production forecast for sunflower seed is 589 000 tons, which is 12,23% less than the previous forecast of 671 100 tons. The revised area estimate for sunflower seed is 529 000 ha (from 559 500 ha the previous month’s estimate), while the expected yield is 1,11 t/ha.

Source: CEC (Crop Estimates Committee)

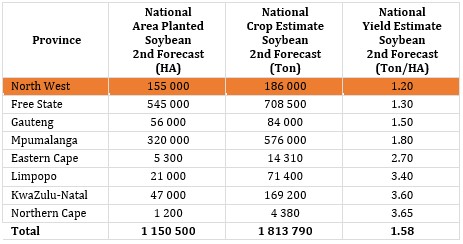

The production forecast for soybeans decreased by 15,22% to 1,814 mills. tons. The estimated area planted to soybeans was revised to 1,151 mills. ha (from 1,122 mill. ha the previous month’s estimate), with an expected yield of 1,58 t/ha.

Source: CEC (Crop Estimates Committee)

Source: CEC (Crop Estimates Committee)

• Imports and exports – national

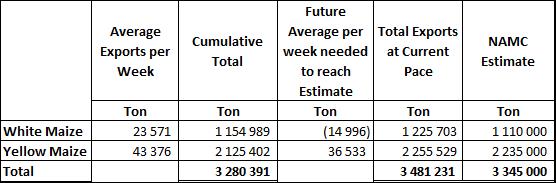

For the production season ending April 2024, 1 154 989 t of white maize and 2 125 402 t of yellow maize have been exported to date (week 49 of 52) as seen in the graphs below.

Source: Sagis

As seen in the table above, the average white maize exports per week are currently 23 571 t. If theoretically, white maize exports remain at the current average per week then there would be 115 703 t more white maize exports than anticipated.

The average yellow maize exports per week are currently 43 376 t. If theoretically, yellow maize exports remain at the current average per week then there would be 20 529 t more yellow maize exports than anticipated.

Source: Sagis

• Parity prices

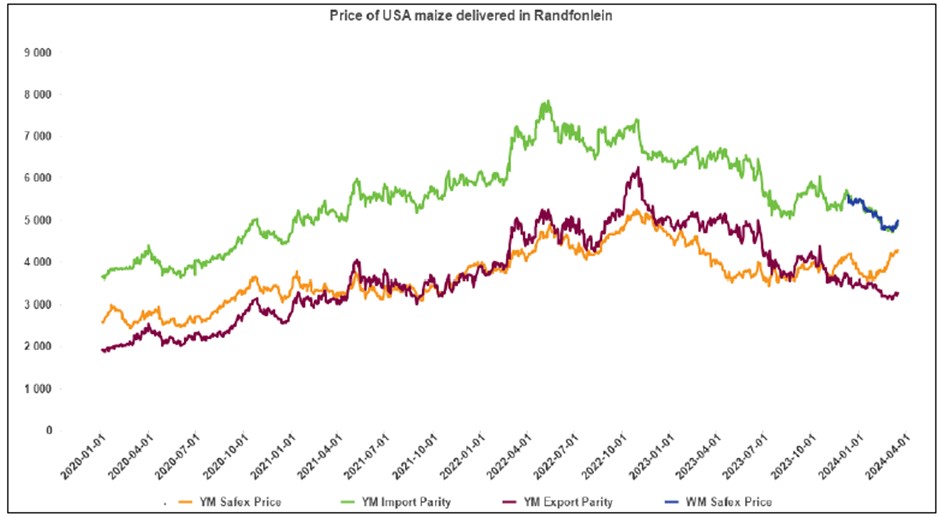

South Africa is a small producer compared to other countries and is thus a price taker (meaning that we cannot influence world prices). Because of this, our local prices are normally between import and export parity, which is illustrated in the figure below. An import parity price is defined as the price which a buyer will pay to buy the product on the world market. This price will include all the costs incurred to get the product delivered to the buyer’s destination.

An export parity price is defined as the price that a local seller could receive by selling his product on the world market e.g., excluding the export costs. The price which the seller obtains is based on the condition that he delivers the product at the nearest export point (usually a harbour) at his own expense.

The graph below reflects the Safex price, import parity and export parity of yellow maize as well as the Safex price of white maize. The import and export parity prices for white maize is not released by Grain SA for this period.

Source: Grain SA

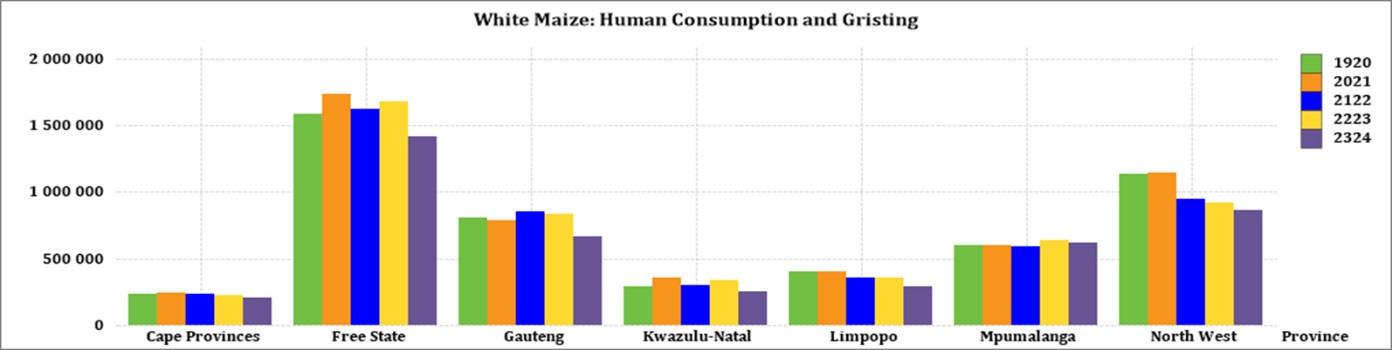

• Grain processing per province

For the marketing year which is May to April (2023/2024), the Free State province dominates the white maize that is used for human consumption and gristing. North West consumed the second most white maize produced for human consumption for the three months November 2023 to January 2024.

Source: Sagis

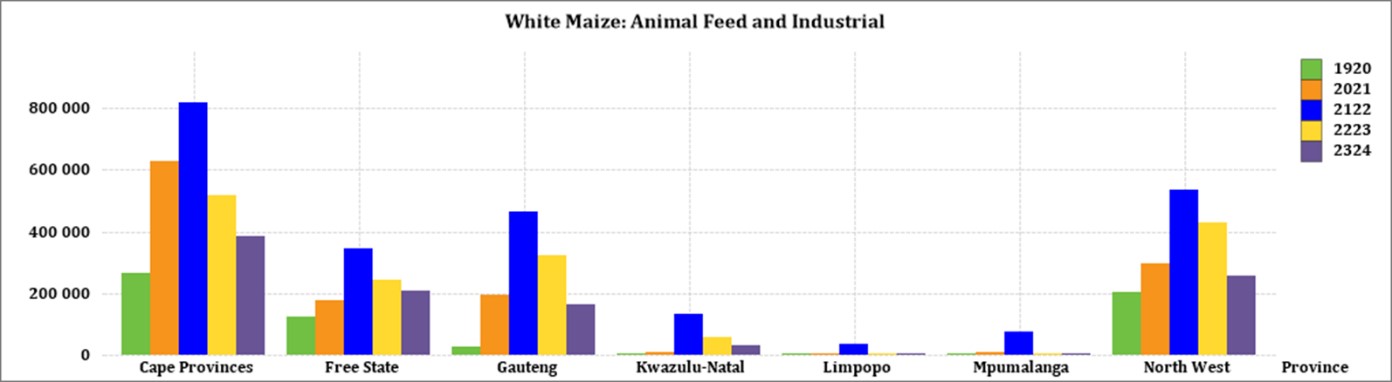

The Free State used the most white maize for animal feed and industrial usage with the Cape Province using the second most.

Source: Sagis

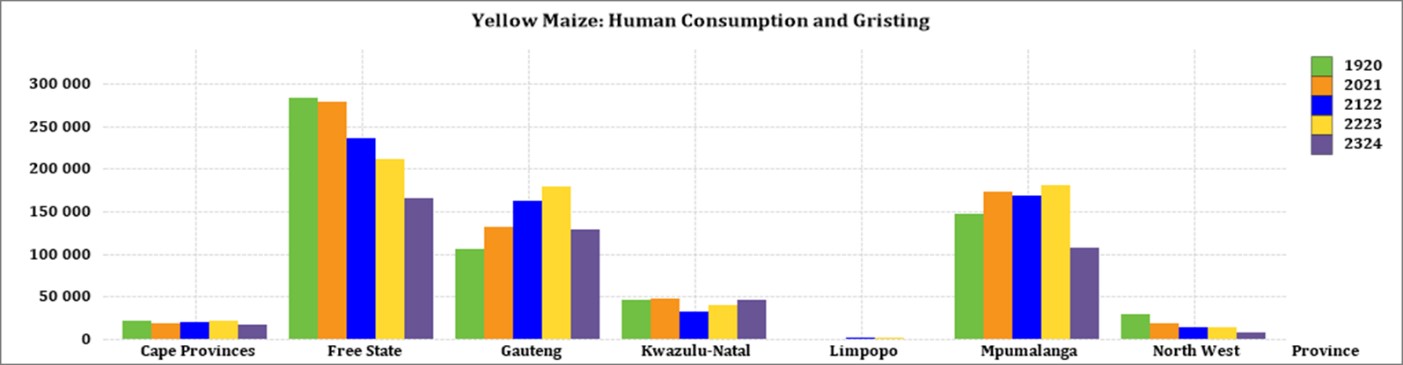

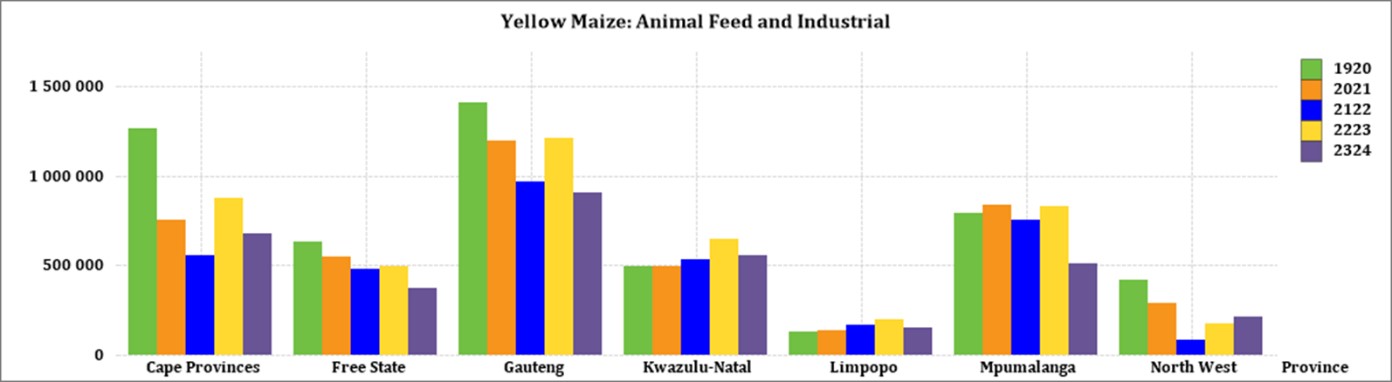

The Free State processed the most yellow maize for consumption and gristing for the three month period November 2023 to January 2024 which is more than for the same period in the previous year. For the same period, Gauteng processed the most yellow maize for animal feed and industrial purposes.

Source: Sagis

Source: Sagis

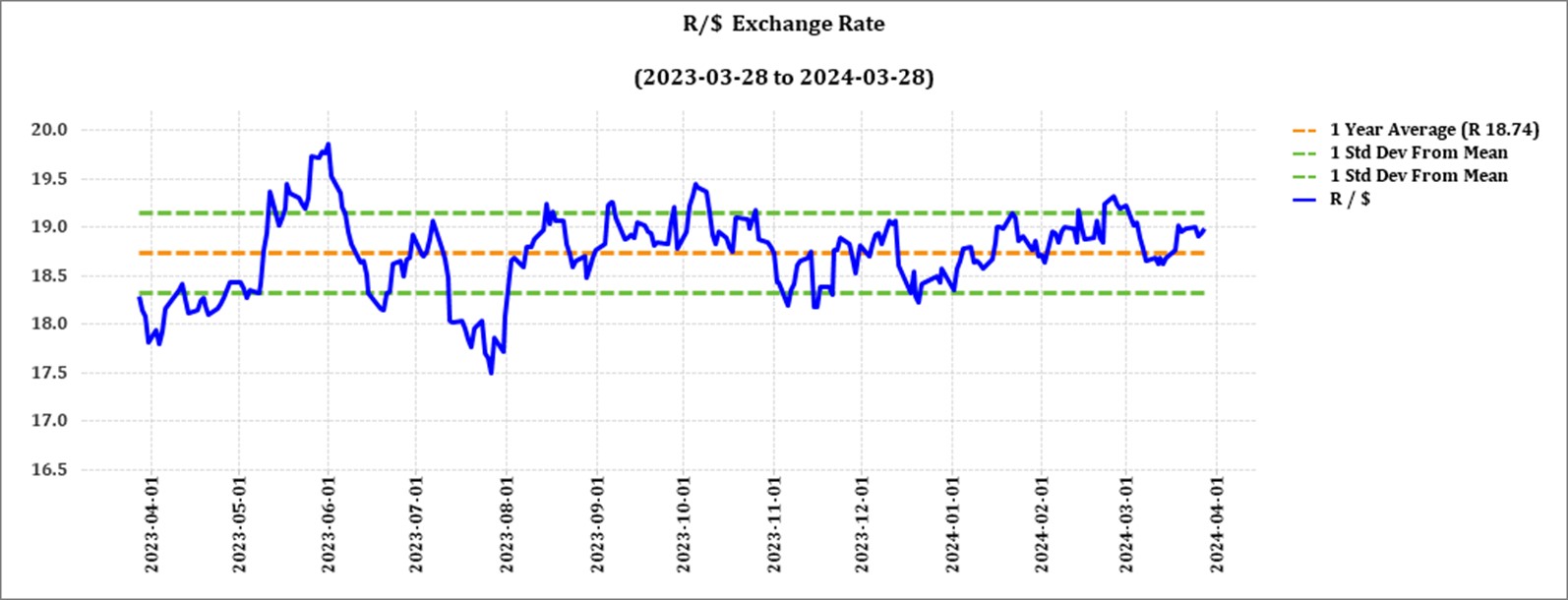

• Exchange rate

NWK Group is exposed to foreign exchange rate risk on various business areas, such as commodity prices and trade imports.

Source: Standard Bank, Corporate and Investment Banking & SARB

On a monthly average basis, the rand appreciated against the US dollar by 0,65% (0,12c) over the period February to March. The one-year average for rand/US dollar as on March 2024 is R18,89. Moreover, the average rand/US dollar exchange rate for March was R18,87 compared to R19,00 in February.

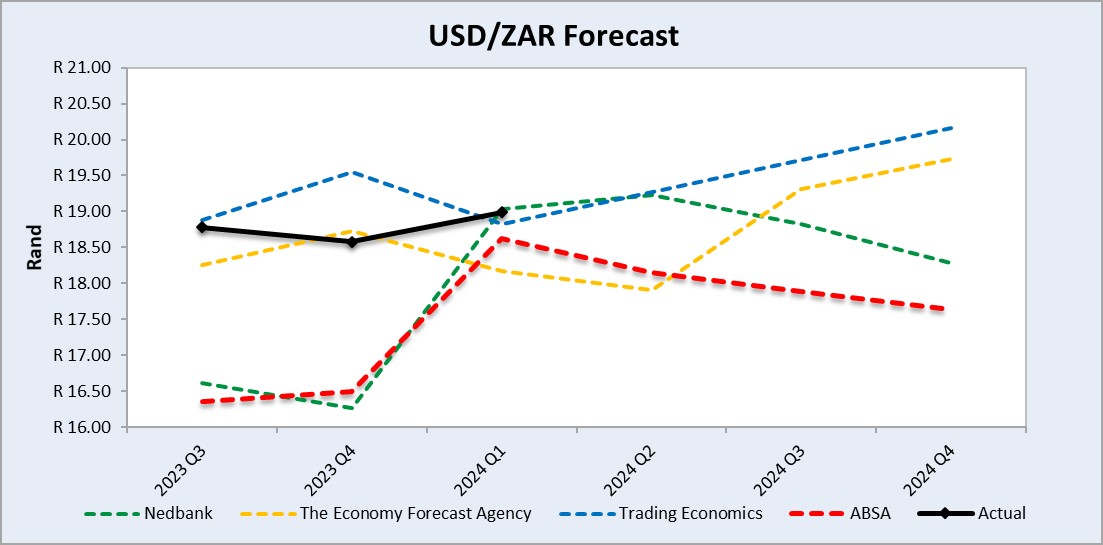

Exchange rate forecast:

Source: Nedbank CIB; Absa; The Economic Forecast Agency; Trading Economics

The graph above shows the actual USD/ZAR for 2023 Quarter 3 (Q3) to 2024 Quarter 4 (Q4) against the forecasted figures.

• Interest rate risk

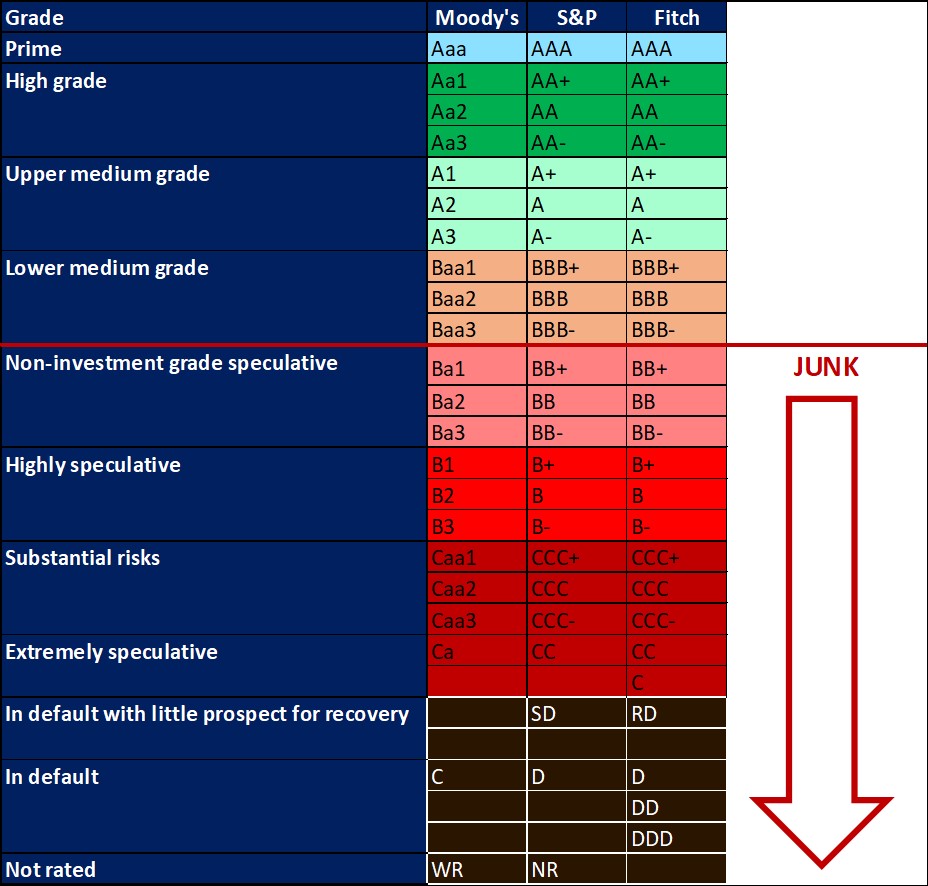

On 27 March 2020, Moody’s downgraded South Africa’s sovereign credit rating to sub-investment grade and placed a negative outlook on the rating. The key drivers for this downgrade include weak economic growth, continuous deterioration in fiscal strength, and slow progress on structural economic reforms. It is now the first time in post-apartheid South Africa that all major rating agencies, i.e., Moody’s, Fitch, and S&P, have South Africa’s credit ratings in sub-investment grade territory. More than a year later and our Moody’s rating remains the same.

During the previous Monetary Policy Committee (MPC) meeting held on 27 March the committee decided that interest rates will remain unchanged. The repo rate is currently 8,25% and the prime rate is 11,75%. The South African Reserve Bank made several interest rates cuts to bring relief to the economy after Covid-19, but since November 2021 borrowing costs rose again by a cumulative 475 bps.

Interest rate movement:

- 22 September 2022: 9,75%

- 24 November 2022: 10,50%

- 26 January 2023: 10,75%

- 30 March 2023: 11,25%

- 25 May 2023: 11,75%

- 20 July 2023: 11,75%

- 21 September 2023: 11,75%

- 23 November: 11,75%

- 27th March 2024: 11,75%

Source: Nedbank CIB; Trading Economics

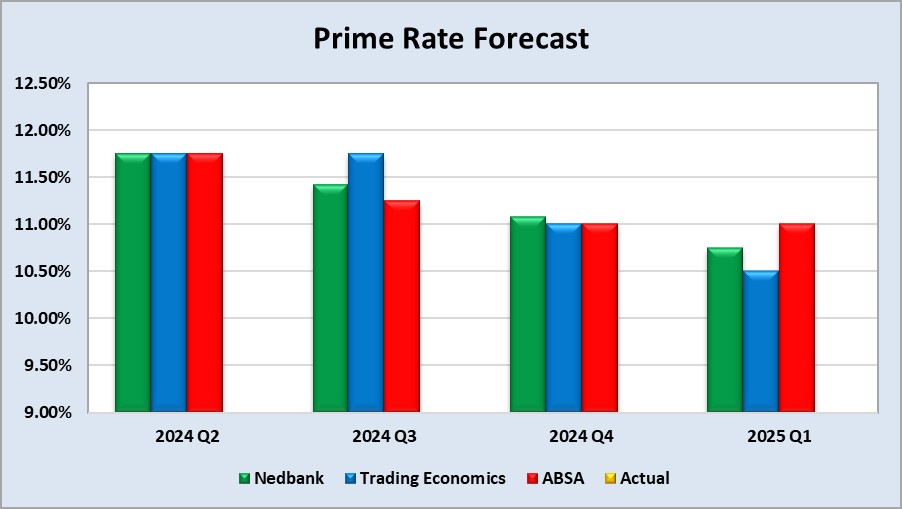

The following graph shows the prime rate forecast for 2024 Quarter 2 to 2025 Quarter 1.

Source: Nedbank CIB; Trading Economics; Absa

As the inflation rate is a driver for increases and decreases in interest rates the current rate and forecast have to be assessed to foresee further increases in the interest rate.

Current

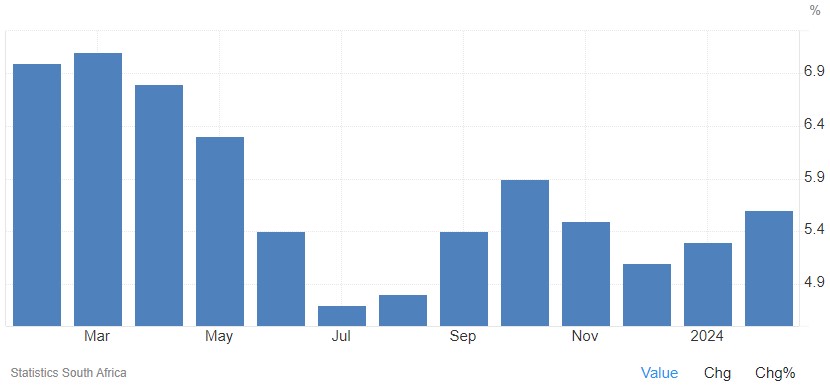

South Africa’s annual inflation rate rose to 5,6% in February 2024, up from January’s 5,3%, slightly above market forecasts of 5,5%, and moving farther from the central bank’s preferred 4,5% midpoint of the 3–6% target range. Main upward pressure came from prices of transportation (+5,4%); housing and utilities (+5,8%) and miscellaneous goods and services (+8,4%). Surprisingly, inflation slowed for food, reaching a two-year low of 6,1% compared to 7,2% in January.

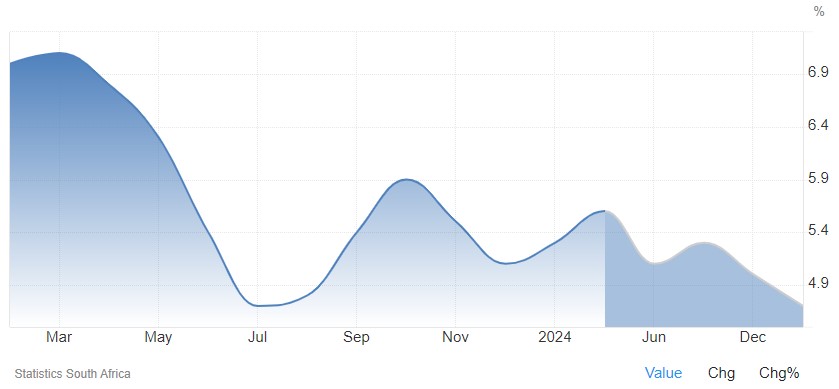

Inflation rate forecast

According to Trading Economics’ global macro models and analysts’ expectations the inflation rate in South Africa is expected to be 5,4% by the end of this quarter. In the long-term, the South Africa Inflation Rate is projected to trend around 4,6% in 2025 and 4,5% in 2026, according to their econometric models.

Source: https://tradingeconomics.com/south-africa/inflation-cpi

• Highlights in the agrochemical sector

China is currently the largest glyphosate supplier in the world. The dynamics of China’s glyphosate greatly impacts the global supply structure, over 80% of glyphosate produced in China is exported, to more than 20 destinations in the world.

In China, the month-to-month analysis reveals a predominantly downward trend in the prices of most herbicides, insecticides, and fungicides in dollar terms from February 2024 to March 2024. Specifically, the tables in this report indicate a 5,5% decrease in the rand terms of glyphosate (95%) during the same period.

The depreciation of the rand over the course of a year influences local prices, causing local prices to not decrease as much as in dollar terms. It is important to note that these international decreases in prices have not been experienced in the local market.

Source: Cnchemicals

Herbicides

The following products are the main products regarding herbicides that may have an impact on input costs for producers.

Glyphosate (95%)

Acetochlor (92%)

Atrazine (97%)

Metolachlor (97%)

Trifluralin (95%)

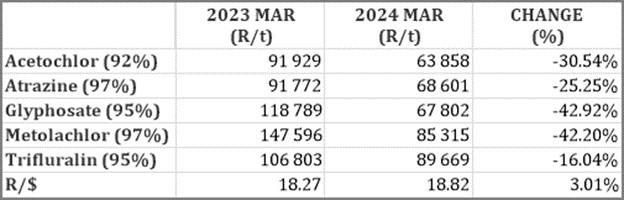

The following comparison is from the April 2024 Grain SA report which reports the previous month’s prices.

In comparison with the previous year’s prices, all of the products experienced a price decrease. Glyphosate had the biggest decrease with 42,9%.

For the two months compared all of the products experienced a price decrease. Trifluralin had the highest decrease of 9,7%.

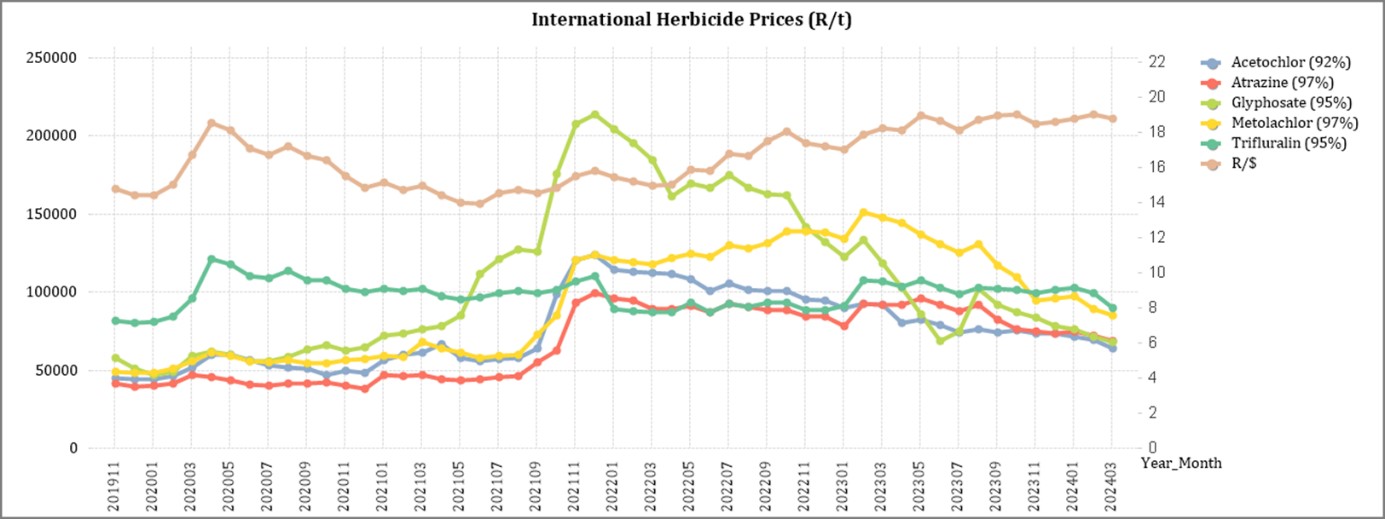

The graph below shows the international herbicides prices (R/t) per product from November 2019 to date.

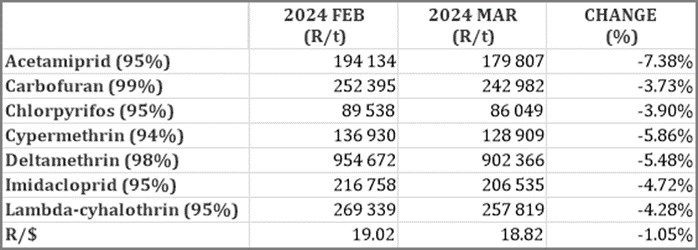

Insecticides

The following products are the main products regarding insecticides that may have an impact on input costs for producers.

Imidacloprid (95%)

Lambda-cyhalothrin (95%)

Carbofuran (99%)

Deltamethrin (98%)

Acetamiprid (95%)

Chlorpyrifos (95%)

Cypermethrin (94%)

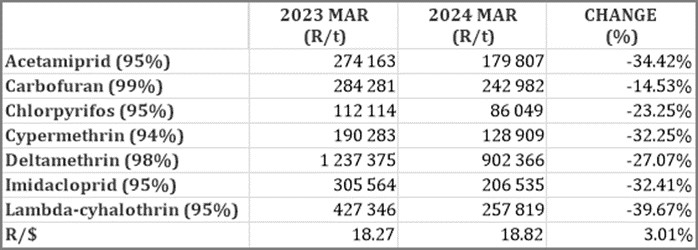

In comparison with the previous year’s prices, all of the products experienced a price decrease. The largest decrease was Lambda-cyhalothrin with 39,7%.

For the two months compared all of the products experienced a price decrease. Acetamiprid had the highest decrease down 7,4%.

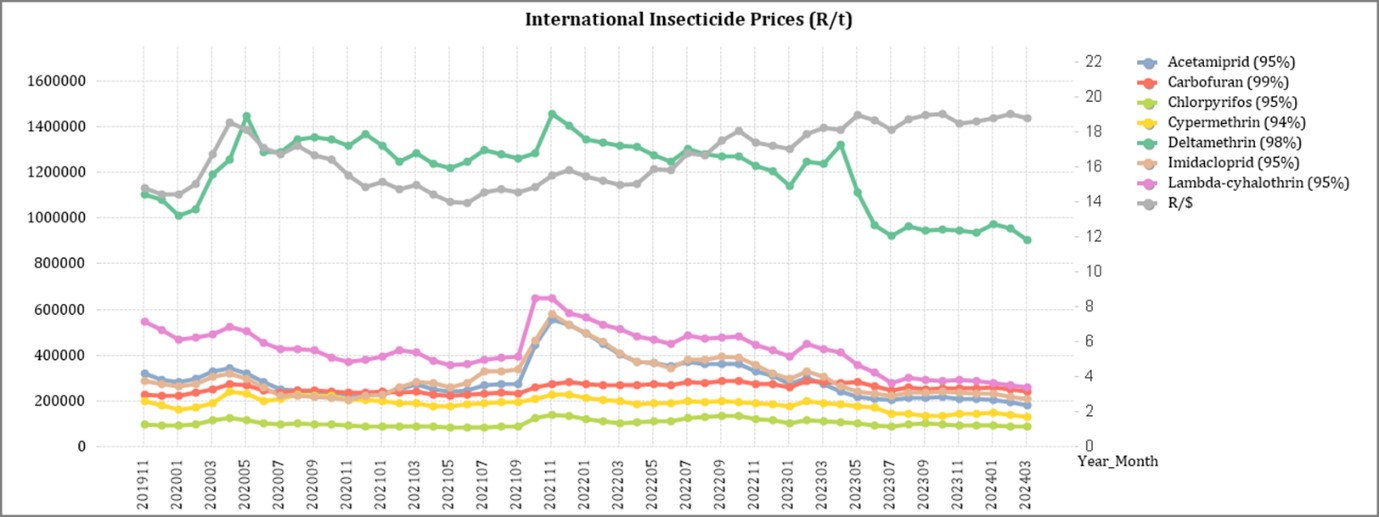

The graph below shows the international insecticide prices (R/t) per product from November 2019 to date.

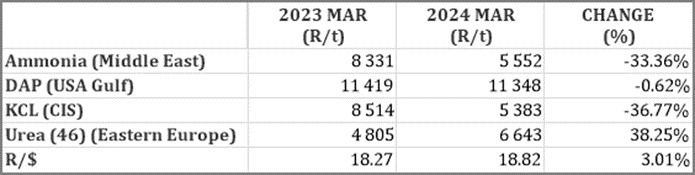

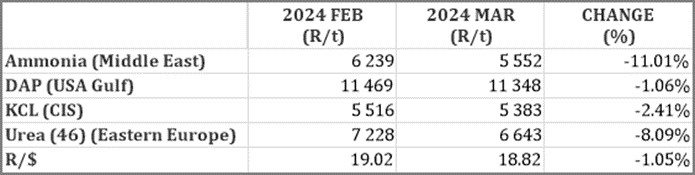

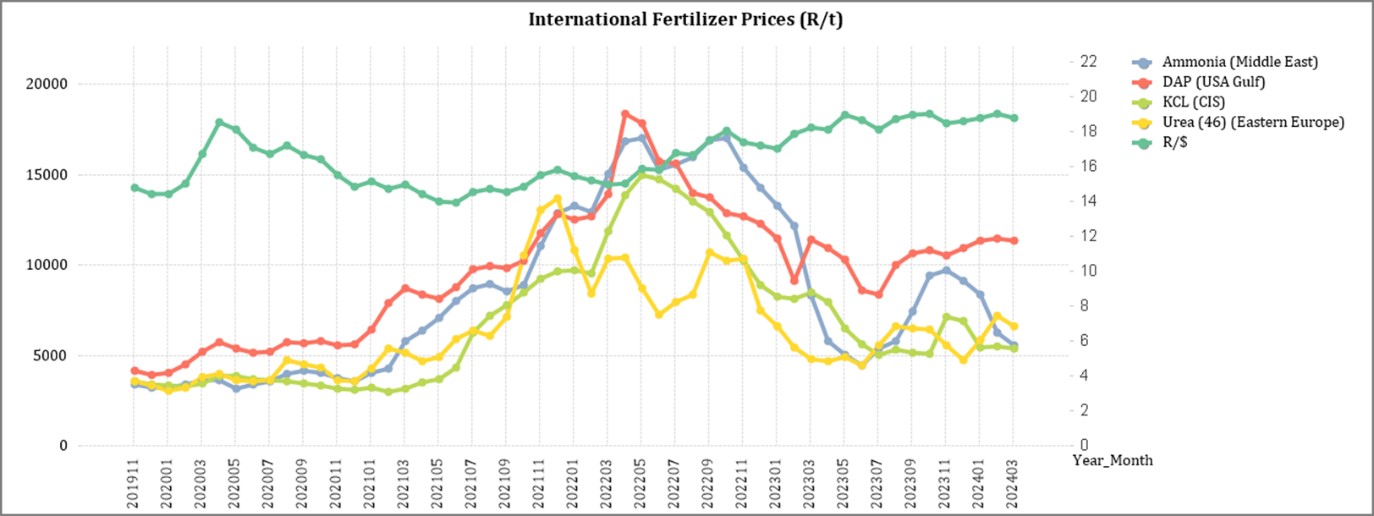

Fertiliser

The following fertiliser products are being analysed:

Ammonia (Middle East)

Urea (46%) (Eastern Europe)

DAP (USA Gulf)

KCL (CIS)

As seen in the table above all three of the main fertiliser products decreased on a year-on-year basis. The biggest decrease, based on average international prices (R/t), was KCL (CIS) (36,77%) followed by ammonia (33,36%). Despite the rest experiencing price decreases, urea had a big price increase of 38,.25% due to lower-than-expected volumes booked on the Indian Urea tender.

For the two months compared all of the products experienced a price decrease. Ammonia had the highest decrease with 11%.

The graph below shows the international fertiliser prices (R/t) per product from November 2019 to date.

Sources: Grain SA – https://www.ft.com/content/4d746aa5-29e3-4796-b9e6-0b64c6865389

Nitrogen: Lower than expected volumes booked on Indian Urea tender send prices plummeting worldwide

Urea: The Indians shocked the urea market by only booking 340 000 t out of the 725 000 t that was offered under the tender. The Indians have the luxury of ample urea stocks in-country and took the view that the lowest price offered under the tender was higher than they were targeting. Needless to add, this move sent urea prices tumbling across all benchmarks.

Ammonia: Ammonia was also quiet this week with all the major price benchmarks unchanged. The market remains split along east-west lines, with the Asian (East) market trading around the $300/t level and prices in the West more in the $450/t to $475/t range.

Phosphates: DAP prices declined again this week and the rate of decline has been sharp enough that Chinese producers are now talking about trying to set a floor price for export DAP. Traders continue to short-sell DAP into India banking on lower DAP prices being available. The Chinese DAP price dropped from $560 to $540/t this week and the Chinese producers are trying to create a minimum price of $530/t FOB China. Given that the global supply-demand balance for phosphates is firmly tilted towards oversupply, it is difficult to see how the Chinese can arrest the price slide other than by cutting back sales/export volumes massively – which is very unlikely at this stage.

Potash: Brazil experienced a small increase in its Potash price as soya demand is said to be driving sales. Soya economics remain unattractive in Brazil, so a sustained recovery in potash prices is unlikely and traders run the risk of Brazil customers cutting back on volumes if they get too ambitious with prices.

Sources

FCurve /F Curve Insight

https://www.grainsa.co.za/upload/report_files/Chemical-and-Fertilizer-Report-April-2024.pdf

Source: GrainSA

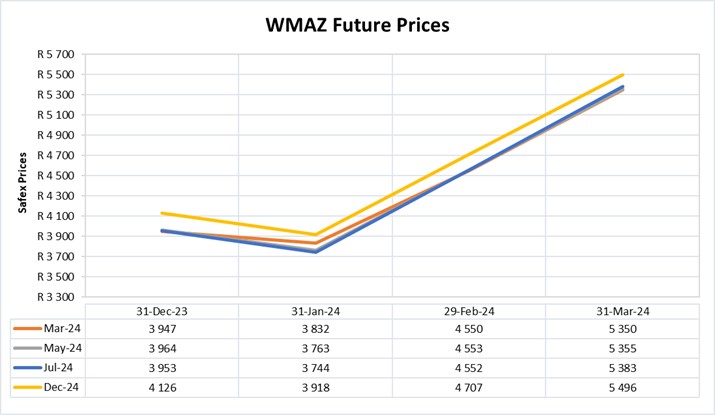

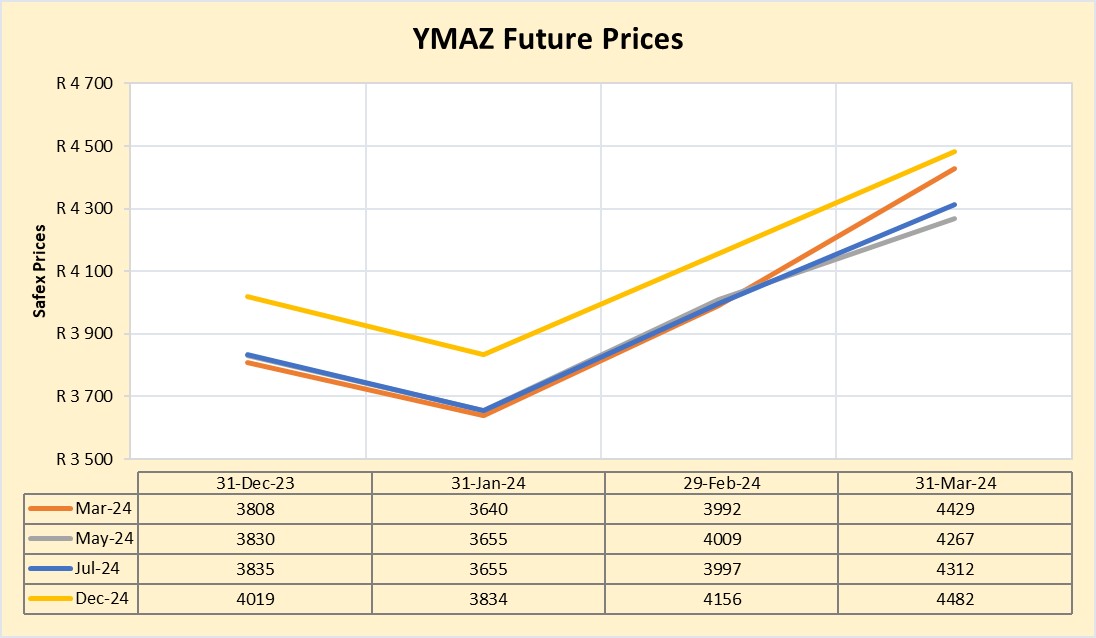

FUTURE PRICES

The graphs below illustrate the market sentiment for maize, in the form of future contracts, for the upcoming contract months. The market sentiment is the expectation of supply and demand fundamentals relating to white and yellow maize in South Africa.

Source: Sagis/JSE

Source: Sagis/JSE

Due to the hotter weather in crop growing regions harvests are struggling. According to Wandile Sihlobo, chief economist at Agbiz, harvest could be down 20% which means that maize products could increase with 10% to 12%.

According to the Crop Estimation Committee grain and oilseed harvest for the current season is down 21% from the previous season.

A worldwide constraint on white maize is expected, but Sihlobo mentioned that yellow maize can be acquired from the world market.

Fraud risk

FRAUD AWARENESS

Fraud.com identified their top ten fraud trends for 2024. Three of the ten risks are mentioned below. The rest will follow in the coming reports.

- Automation: Fraudsters use software and bots to accomplish tasks. Automation makes it easier for them to remain undetected and cover more ground. This increases the risk of fraud. For example, credential stuffing is the act of testing stolen or leaked credentials on websites and services at scale to see if they work on any accounts.

- Account takeover: In a typical account takeover attack, hackers use malware and phishing methods to acquire legitimate user credentials or buy them from the dark web. They then use these stolen credentials to take over your accounts (personal or business). This includes email, bank and other accounts.

- Adoption of New Digital Payments and Methods: This allows consumers and businesses to make payments more quickly and efficiently, but they also open new avenues of attack from fraudsters as they use stolen credentials to carry out fraud and identity theft. Cryptocurrencies are growing in popularity and the anonymity provided by these currencies makes it easy for criminals to carry out illicit activities.

Source: https://www.fraud.com/post/top-10-fraud-identity-theft-trends

{kind=link}